Board of Director's Report

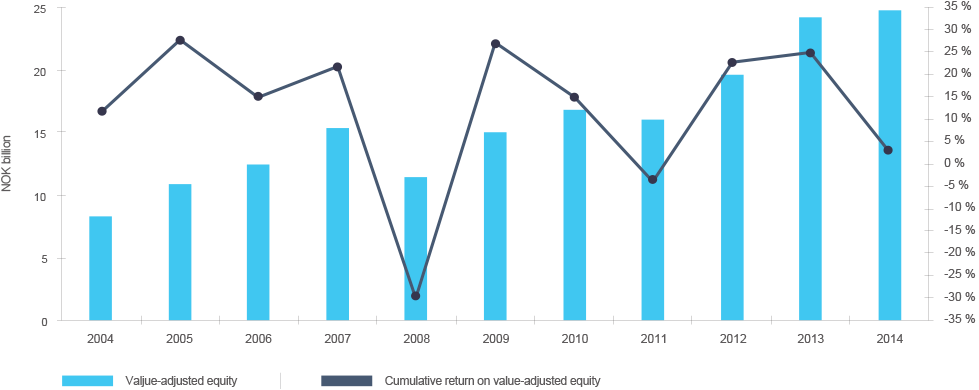

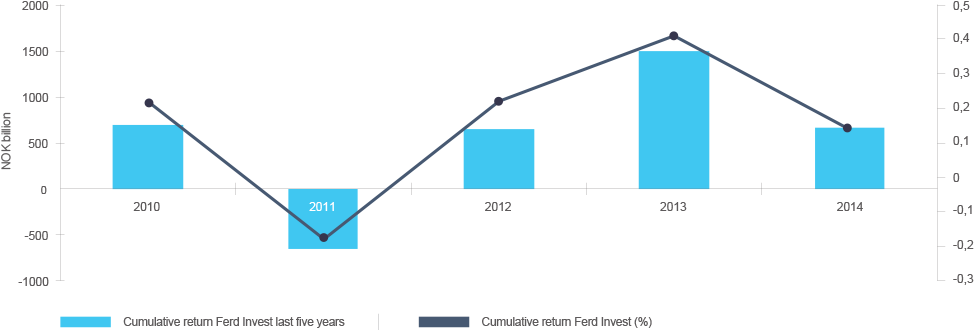

2014 was a year in which Ferd's business areas reported variable results. Three areas achieved a good absolute return, but the performance of Ferd's oil service companies and Elopak resulted in Ferd Capital reporting a negative return for the year. In total, Ferd generated a return of approximately NOK 700 million or 2.9% in 2014. Ferd's performance in 2014 was weaker than the return achieved on the Oslo Stock Exchange, and also fell short of our expectations. Ferd's average annual return over the last five years was 12.1%, which is significantly better than the return for the Oslo Stock Exchange but weaker than the global stock market index in Norwegian krone terms (MSCI). At the close of 2014, Ferd's value adjusted equity was NOK 24.9 billion.

2014 was a year in which Ferd's business areas reported variable results.

Long-term interest rates fell in 2014, both in Norway and internationally. The decline in activity seen in the oil industry was an important factor in the decision by the Norwegian central bank to cut its key policy rate. The Norwegian krone depreciated significantly, particularly against the US dollar but also against the euro. Just under 40% of Ferd's investments are denominated in Norwegian krone, with 25% in US dollar and 25% in euro. Ferd recorded a currency gain of over NOK 1 billion in 2014. Stock markets in industrialised countries generally had a good performance in 2014. However, the Norwegian stock market only managed a 5% gain for the year as the result of a 40% decline in the oil service index.

Ferd's average annual return over the last five years was 12.1%, which is significantly better than the return for the Oslo Stock Exchange but weaker than the global stock market index in Norwegian krone terms (MSCI).

In January 2014, Ferd increased its ownership interest in Interwell from 34% to 58%. Towards the end of 2014, Ferd Capital purchased 10.1% of Petroleum Geo-Services, a stock exchange listed seismic company. Ferd Real Estate invested approximately NOK 400 million in new real estate assets and existing projects over the course of 2014. Ferd and the funds in which Ferd are invested in realised sizeable disposals in 2014. Ferd Special Investments and Ferd's investments in Private Equity funds generated cash from disposals of almost NOK 1.6 billion. At the close of 2014, Ferd AS (parent company) had credit facilities available on the group's facility of NOK 5.5 billion. Ferd accordingly now has considerable capital resources available for new investments in the future.

Future prospects

A modest upswing in the global economy is expected in 2015. The outlook for securities markets will depend in part on the extent to which central banks continue to implement expansive monetary policy measures. The American central bank is now cutting back on quantitative easing, but the Eurozone economy is still in need of monetary policy stimulus. There is a lower level of activity in the oil sector in Norway, but the weakness of the Norwegian krone may lead to stronger growth for the mainland Norwegian economy. The Norwegian central bank is expected to make one or possibly two further cuts in Norwegian interest rates over the course of 2015. The area of greatest uncertainty is the extent to which the low level of activity in the oil sector will affect the overall Norwegian economy. Given the current level of pricing seen in stock markets, particularly in the USA, continuing growth in corporate earnings will be needed if the market outlook is to remain positive. This in turn means that in order for stock markets to continue to generate a good return, it is essential that the American economy maintains its growth and that European economies show further improvement.

Until now, Ferd Capital's investments have, with just two exceptions, been in unlisted companies. It has now been decided that Ferd Capital will consider new investments in both listed and unlisted companies. When assessing investment opportunities, Ferd Capital's decisions depend principally on its evaluation of company-specific factors. In the business areas responsible for financial investments, interest is focused on finding investment opportunities where the current valuation in the market permits a favourable potential return at an acceptable level of risk.

Over the last ten years, Ferd has generated a total return of NOK 18.0 billion, equivalent to an annual return of 12.6%.

The group's value-adjusted equity

Over the last ten years, Ferd has generated a total return of NOK 18.0 billion, equivalent to an annual return of 12.6%. Ferd evaluates its return on the basis of the absolute return achieved over time and how this relates to the level of risk exposure that has been involved.

Some of the companies in Ferd Capital’s portfolio performed well in 2014, but Aibel and Elopak reported weak performance for the year.

Ferd holds a broadly diversified portfolio of listed and unlisted equity investments, alternative investments and real estate. Ferd's equity investments provide good diversification between different sectors and geographical markets and between companies at different stages of the corporate life cycle. Ferd Capital’s portfolio represents just under 40% of Ferd’s value-adjusted equity.

Some of the companies in Ferd Capital’s portfolio performed well in 2014, but Aibel and Elopak reported weak performance for the year. Ferd Invest’s Nordic share portfolio generated a return of 14%, which was one percentage point lower than the return on the benchmark index for this portfolio. Ferd Special Investments also reported a good absolute return.

Ferd Hedge Funds reported a satisfactory relative return in 2014. The return on the hedge fund portfolio was 4%, while Ferd's real estate portfolio achieved a return of 15%. The good return achieved by Ferd Real Estate was the result of both strong returns on certain individual projects and the general performance of the real estate market in 2014.

Financial results for Ferd AS

Ferd AS is an investment company with investments in a broad range of asset classes. The registered office of Ferd AS is at Lysaker in Bærum municipality. Recognition of assets at fair value is of key importance for an investment company, and Ferd accordingly presents accounts that report its investments at fair value, including the subsidiary companies of Ferd AS.

Ferd AS reports operating profit of NOK 584 million for 2014, representing a decrease of NOK 4,906 million from 2013. In addition to the matters mentioned above, the most important reason for the profit reported for 2014 was the weak return from investments in Private Equity funds.

Net cash flow for 2014 was made up of cash from operations of NOK -250 million, NOK -3 million from investment activities and NOK 350 million from financing activities.

For further commentary on financial results in 2014, the reader is referred to the separate sections on each business area on the following pages.

The annual accounts have been prepared on the going concern assumption, and in accordance with Section 3-3a of the Accounting Act, the Board confirms that the going concern assumption is appropriate.

Financial results and cash flow for Ferd (Ferd AS group)

Operating revenue was NOK 14.0 billion in 2014, in line with 2013. In 2013 Ferd recognised to income NOK 3.0 billion in respect of the increased value of shares and equity participations, while in 2014 Ferd earned NOK 0.6 billion from its financial investments.

Sales revenue increased from NOK 11.0 billion in 2013 to NOK 13.1 billion in 2014. Consolidated sales revenue reported by Ferd includes the revenue reported by Servi Group for the whole of 2014, while in 2013 Servi Group's revenue was included from August. Elopak reported operating revenue of NOK 6.5 billion in 2014, up by NOK 0.5 billion from the previous year. Elopak’s revenue is denominated in euro, and the increase in revenue reported for 2014 was due in part to the weakness of the Norwegian krone and in part to slightly higher revenue. Mestergruppen reported an increase in revenue of NOK 0.2 billion in 2014 compared to 2013. In addition, consolidated sales revenue reported by Ferd for 2014 includes NOK 0.9 billion of revenue reported by Interwell, which was consolidated from January 2014.

Ferd is committed to innovation, and the group's research and development activities are principally carried out in subsidiary companies, where almost NOK 150 million of development costs were recognised to profit and loss in 2014. In addition, a number of development projects have been capitalised to the balance sheet as intangible assets, representing almost NOK 500 million of capitalised developed expenses as well as new patents and other intellectual property rights.

The group’s financial items showed net income of NOK 3 million in 2014 compared to net financial expense of NOK 512 million in 2013. This improvement is principally due to currency effects.

Ferd normally has a low effective tax rate because a large part of its earnings is generated from investments in shares. Under the exemption model, gains on shares are not taxable. However, many taxable gains were realised in 2014, and the effective tax rate for the year was 34.1%. The group’s net tax charge for 2014 was NOK 490 million as compared to a charge of NOK 267 million for 2013.

Net cash flow for 2014 was made up of cash from operations of NOK 928 million, cash from investment activities of NOK -1,389 million, and cash from financing activities of NOK 428 million. The most important factor in the positive cash flow from financing activities was the drawdown of borrowings by the parent company Ferd AS.

Strategy

The overall vision for Ferd’s activities is to ‘create enduring value and leave clear footprints’. Ferd’s corporate mission statement states that the group will hold a combination of industrial investments where Ferd has ownership positions that give it a significant influence and financial portfolios that represent diversification for Ferd. Ferd will accordingly strive to maximise its value-adjusted equity capital over time.

The approach to risk exposure taken by the owner and the Board of Directors is one of the most important parameters for Ferd’s activities. This defines Ferd’s risk-bearing capacity, which is an expression of the maximum risk exposure permitted across the composition of Ferd’s overall portfolio. Ferd’s risk willingness, which determines how much of its risk-bearing capacity should be used, will vary over time, reflecting both the availability of attractive investment opportunities and the company’s view on general market conditions.

The Board keeps Ferd's risk capacity under continuous review. The assessment of how Ferd's risk capital is allocated represents one of the Board’s most important tasks, since risk exposure and return are largely determined by the assets in which Ferd invests. The allocation of new capital, as well as the reallocation of capital between business areas, represents a systematic approach to making use of the group's capital base and risk-bearing capacity.

It is Ferd’s intention that its allocation of capital should be characterised by a high equity exposure and good risk diversification. Good risk diversification helps to ensure that Ferd can maintain its exposure to equity investments, even at times when other players have less access to capital. In addition, maintaining strong liquidity enables us to maintain our freedom to operate as we wish even in more difficult times.

Ferd’s equity capital investments represent a well-diversified portfolio, and the overall performance shows a relatively strong correlation with the performance of Norwegian and international stock markets. Ferd Real Estate and Ferd Hedge Funds help to reduce the group’s overall risk exposure because these investments involve less risk than investing in equities.

Asset allocation must be consistent with the owner’s willingness and ability to assume risk. This provides guidance on how large a proportion of equity can be invested in asset classes with a high risk of fall in value. The risk of fall in value is measured and monitored with the help of stress testing. The risk of fall in value at the start of 2015 was a little lower than both the average risk for 2014 and the average risk over the last five years.

Ferd aims to maintain sound creditworthiness at all times in order to ensure that it has freedom of manoeuvre and can readily access low-cost financing at short notice when it wishes. Ferd's objective is that its main banking connections will rate Ferd’s creditworthiness as equivalent to ‘investment grade’. In order to protect Ferd’s other equity from risk, Ferd Capital and Ferd Real Estate carry out their investments as stand-alone projects without guarantees from Ferd. Both Ferd and its banks pay close attention to liquidity. Ferd has always held liquidity comfortably in excess of the minimum liquidity requirements we impose internally and the requirements to which we are committed by loan agreements at the parent company level. Ferd works on the assumption that the return generated by financial investments should help to cover current interest payments. It is also important that the balance sheet is liquid, and that the maturity profile of assets corresponds closely to the maturity profile of liabilities.

Ferd has a proactive approach to currency exposure. We work on the assumption that Ferd will always have a certain proportion of its equity invested in euro, US dollar and Swedish krona denominated investments, and accordingly do not normally hedge currency exposure against the Norwegian krone. If the exposure to any one currency is judged to be too great or too small, the currency exposure is adjusted by borrowing in the currency in question at the parent company level, or by using derivatives.

Ferd holds only very limited investments in interest-bearing securities. Its exposure to interest rate risk arises from any borrowing that may have been drawn down, and is managed by group treasury.

Further information on Ferd’s strategy can be found in a separate article.

Corporate Governance

Ferd is a relatively large corporate group, with a single controlling owner. Despite this, the Board of Directors of Ferd Holding AS has substantially the same responsibilities and authority as the board of a public company.

Not all the sections of the Norwegian Code of Practice for Corporate Governance are relevant to a family-owned company such as Ferd, but Ferd complies with the Code where it is relevant and applicable. Further information is provided in a separate article on corporate governance. The Board of Directors of Ferd Holding held seven Board meetings in 2014.

Ferd Capital

When making investment decisions, Ferd Capital attaches only little weight to the overall macroeconomic outlook. Company-specific factors play the crucial role when deciding whether or not investment opportunities are attractive. In December 2014, Ferd Capital built up a 10.1% stake in the stock exchange listed seismic company Petroleum Geo-Services, becoming its single largest shareholder. Ferd Capital’s aim is to contribute actively to growing the company further. In January 2014, Ferd capital increased its ownership interest in Interwell from 34% to 58%.

Ferd Capital sold its ownership interests in venture capital businesses to Verdane Capital VIII K/S in 2014. Following this disposal, Ferd Capital no longer holds any investments in the venture capital segment that are owned directly by Ferd.

Aibel

Aibel is a supplier of services related to oil, gas and renewable energy. The company is one of the largest Norwegian oil service companies involved in engineering design, construction, maintenance and modification of oil and gas production facilities for the upstream oil and gas industry.

Aibel reported turnover of NOK 8,554 million in 2014 as compared to NOK 12,645 million in 2013. EBITDA was NOK 184 million as compared to NOK 778 million in 2013.

At the start of 2014, Statoil indicated to Aibel that it wished to reduce the volume of activity to be carried out under its framework contract. In addition, Statoil intended to reduce or defer new modification assignments. The large fall in the oil price seen over the course of the second half of the year made market conditions even more challenging.

Aibel experienced a drop of around 25% in the volume of maintenance and modification contracts between 2013 and 2014. The new building market also saw a significant slowdown, and these developments meant that 2014 was a year of adjustments for the company. Aibel was one of the first companies in the industry to make capacity adjustments, which included significantly reducing the use of hired-in workers and employee numbers. In order to improve its competitiveness, the company took action to improve its efficiency and reduce its cost base. Ferd contributed NOK 50 million of new equity in July 2014 in order to strengthen Aibel's financial condition.

Aibel expects market conditions to remain challenging in 2015, although the market is expected to improve over the medium term. The increasing number of platforms on the Norwegian continental shelf and ageing of existing platforms will create greater demand for maintenance and modification work. In addition, fields such as Johan Sverdrup will lead to significant investment in the Norwegian continental shelf in the years ahead. Aibel was awarded a contract in February 2015 for construction of the deck of the drilling platform for the Johan Sverdrup field.

Aibel’s ambition going forward is to use the challenging market conditions to strengthen its position as one of the leading oil service companies for oil and gas on the Norwegian continental shelf by further enhancing the company’s competitiveness and thereby positioning the company for new growth.

Elopak

Elopak is a supplier of packaging systems for liquid food products. The company is a total system supplier, developing carton packaging solutions for both fresh and aseptic products.

Elopak’s business is in general less cyclical than many other industries, and should therefore not experience any major loss of volume as a result of changes in economic conditions. However, the company expects carton sales for the juice market to be more volatile. Demand for these products is affected both by the state of consumers' finances and changing preferences between juices and competing beverage products.

Elopak’s total revenue was NOK 6,471 million in 2014, compared to NOK 5,967 million in 2013. The increase in reported revenue was the result of a higher average euro exchange rate in 2014 than in 2013 and slightly higher revenue. Elopak's euro-denominated reported revenue in 2014 was EUR 776 million as compared to EUR 769 million in 2013.

Elopak reports EBITDA of NOK 612 million for 2014, as compared to NOK 651 million in 2013. The main reason for the reported decrease was the increase in costs caused by significant investment in growth initiatives.

Elopak made major investments in 2013 in establishing EloBrickTM (roll-feed aseptic carton packaging) as a separate business area, with the associated organisational structure and production facilities. Elopak continued to invest in EloBrick in 2014, and completed the expansion of its production capacity. The commercial rollout of EloBrick to Elopak's customers is now fully underway. Elopak also continued its strategy for growth in the aseptic packaging market. The new aseptic filling machinery has been approved as a system for use by customers that sell juice products, and commercial sales have commenced.

The company decided in 2013 to upgrade and expand its production capacity in Canada, and production will be transferred to a new facility in Montreal. Construction of the new facility is proceeding according to plan. The transfer of production will start in mid-2015, and the new facility will reach full production capacity during the course of 2016.

The markets for Elopak’s products are expected to be relatively stable compared to the 2014. However, the outlook for the Russian market is uncertain due to the current economic and political situation.

The Board is of the opinion that Elopak will position to meet the challenges the group faces. Elopak will continue to pursue its growth strategy in the aseptic segment in 2015.

Interwell

Interwell is a leading Norwegian supplier of high-technology well solutions for the international oil and gas industry. The company’s most important market is the Norwegian continental shelf. In recent years, Interwell has also expanded its presence in a number of important international markets in Europe, the Middle East and the USA.

Despite the fall in the price of oil and the cash flow challenges this caused for oil companies in 2014, Interwell reported another year of strong organic growth. The company achieved significant growth in both the Middle East and the USA, and it continued to make good progress in regions where it is more established.

Interwell reported revenue of NOK 856 million in 2014, an increase of 14% from 2013. EBITDA for 2014 was NOK 315 million, up by 18% from 2013.

There is significant uncertainty in the market given the oil price and the cash flow challenges faced by oil companies as we go into 2015. Despite this, Interwell is well-positioned to achieve underlying growth. Interwell principally delivers services to the well intervention market, which has historically been less influenced by the cyclicality of the oil services market, and the company’s services and products help improve oil companies’ cash flows. The company has built a robust international platform and therefore has limited exposure if a particular region happens to experience a period of weak growth.

Interwell remains committed to being a technological leader in its niche areas, and will continue its strong focus on continuous technological development in the years ahead. In today’s market, developing technology that is able to further help oil companies increase their revenue and reduce their costs is critical for Interwell.

Telecomputing

TeleComputing is a leading provider of complete IT services to the Nordic small and medium enterprise (SME) market.

TeleComputing reported EBITDA of NOK 224 million in 2014, representing a modest improvement from 2013. TeleComputing's revenue increased by 5% in 2014, which is a higher rate of growth than the IT market as whole but is below the company's long-term target. As the consulting activities carried out by the subsidiary company Kentor also saw increased demand in relation to the company’s services in the second half of the year, TeleComputing is now in a situation where all business areas reported year-on-year growth.

TeleComputing was again successful in renewing many important contracts in 2014, as well as in attracting many new customers. This resulted in a larger order backlog at the end of 2014 than at any other point in the company’s history. TeleComputing's objective is to maintain industry-leading margins. This was again achieved in 2014. A particularly positive point was that both business areas in Sweden reported improved profit margins.

The IT operations business is expected to grow well going forward, supported by the record-high order backlog. The company is uniquely positioned in the Scandinavian market to help customers reap the benefits of cloud-based IT services.

Mestergruppen

Mestergruppen is a leading supplier of building products for the B2B market.

Mestergruppen reported revenue from its building products activities in 2014 of NOK 2,698 million, representing growth of 5% compared to 2013. Mestergruppen focused in 2014 on streamlining the company's organisational structure and improving efficiency.

There is uncertainty about how the building materials market will play out in 2015. In the medium term, the building materials industry is expected to grow on average approximately in line with the historic trend. The building materials industry in Norway is fragmented, competitive and exposed to economic cycles. Mestergruppen will continue its focus on creating profitable growth through increased volume, operational efficiency and efficient flow of goods through the whole value chain. Ferd’s ambition is to strengthen Mestergruppen’s position as a cost leader in the building materials industry in Norway.

Swix Sport

Swix Sport develops, produces and markets innovative and high-quality products for sporting and other active recreational pursuits, both in Norway and internationally.

Revenue increased from NOK 757 million in 2013 to NOK 813 million in 2014. Sales in Sweden have been very strong and very good results have been achieved by these activities following Swix’s decision in 2013 to take over sales and distribution in the Swedish market. In 2014, approximately 50% of Swix’s revenue was generated outside of Norway. Swix operates through two main divisions, Sport (Swix and Toko) and Outdoor (Ulvang and Lundhags) in order to emphasise its focus on the outdoor segment. Swix Sport reported EBITDA of NOK 58 million for 2014 as compared to NOK 71 million in 2013. The decline in earnings was the result of higher distribution costs in 2014, due in part to the weakness of the Norwegian krone.

The continuing trend for greater interest in health and outdoor pursuits offers good future prospects for the sporting goods industry in general, and Swix Sport in particular. Swix's objective is to place greater focus on the outdoor segment using the Lundhags and Ulvang brands to reduce seasonal variation in its revenue, while at the same time ensuring that Swix maintains its position as a global leader in winter sports.

The sporting goods market remains highly competitive, and continuous innovation combined with efficient distribution are key to winning market share.

Servi Group

Servi develops and produces customer-specific hydraulic systems, cylinders and valves for offshore, maritime and land-based industries.

Servi Group reported revenue of NOK 883 million in 2014 as compared to NOK 855 million in 2013, making 2014 a record year for the company. This was principally due to a high level of activity in the marine and offshore segment.

EBITDA for 2014 was NOK 113 million as compared to NOK 76 million in 2013. After correcting for non-recurring items, Servi's profit for 2014 was little changed from 2013.

Servi is well-positioned for continuing organic growth, but demand from the oil industry is expected to be weaker in 2015. The company is seeing a healthy flow of orders from its largest customers in other segments, with a continuing positive trend. Servi has established a new organisation in Houston, which has given the company a better starting point to attract new customers in the American market. In addition, the Houston office will enable Servi to extend its service for existing Norwegian customers in the American market.

Servi’s objective is to be the market leader and preferred hydraulics partner for its customers. The company places great importance on closeness to its customers, combined with continuous development of its technology and services, in order to maintain its market-leading position.

Ferd Invest

Ferd Invest invests in listed Nordic shares. Its target is to generate a return that is higher than the return on its Nordic benchmark index. The investment team does not focus on country or sector allocation, or on the constituents of the benchmark index.

Ferd Invest reported an operating profit of NOK 657 million as compared to NOK 1,471 million in 2013. 2014 was another year in which Nordic stock markets delivered positive returns. Share prices rose by less than in 2013, but Nordic stock markets gained between 21% (Copenhagen) and 5% (Oslo) in local currency terms. When these rises are measured in Norwegian krone terms, they are even greater.

The market value of the Ferd Invest portfolio grew by 13.9% in 2014, which was 1.3 percentage points weaker than the benchmark index for the portfolio. Ferd Invest's most successful investments in 2014 were Outokumpu, Autoliv, Kone and Novo Nordisk. The investments with the weakest performance in 2014 were in the energy sector and companies exposed to the Russian economy.

At the close of 2014, the market value of the Ferd Invest portfolio was NOK 5.2 billion. Investments are divided between the three Scandinavian stock markets, in addition to the Helsinki stock market. The largest investments at the close of 2014 were in Opera Software, Autoliv, Kone OY, Assa Abloy and Hexagon. These investments accounted for around 40% of the total value of the portfolio at year-end.

Ferd Hedge Fund

Ferd’s objective for its hedge fund portfolio is to achieve a satisfactory risk-adjusted return over time, both relative to the market and in absolute terms. In order to achieve good risk diversification, it is important that the composition of the portfolio features a range of funds which generate returns that are not dependent on the same risk factors. In addition, as part of risk diversification for Ferd’s overall portfolio, the hedge fund portfolio normally has a relatively small weighting in funds that are heavily exposed to the stock market.

Ferd Hedge Fund’s portfolio achieved a return of 3.5% in 2014, which was 0.4 percentage point higher than the return for the benchmark index against which the performance of the portfolio is measured. The return for the year was NOK 103 million. The market value of the portfolio at the end of 2014 was NOK 2.9 billion.

While changes to the hedge fund portfolio were on a moderate scale in 2013, 2014 was a more active year with many adjustments to the portfolio. Over the course of the year, Ferd Hedge Fund worked to concentrate the portfolio by reducing the number of funds in which it is invested. The number of funds has decreased from 26 to 20, and the concentration of the portfolio on the 10 largest positions also increased during the course of the year.

The objective for the hedge fund portfolio is still to maintain a well-diversified portfolio, but the purpose of the changes is to ensure that Ferd Hedge Fund generates a better reward for making good choices of fund managers.

Ferd Special Investments

The investment mandate for ‘Special Investments’ was put in place in spring 2010, and Special Investments became a separate business area in autumn 2012. The objective for this business area is to benefit from investment opportunities that Ferd is well placed both to evaluate and to hold, but which fall outside the group’s other mandates.

Investments held in this portfolio share the common feature of a favourable balance between the potential return and the risk of loss. Particular attention is paid to being able to identify good protection against downside risk. It has so far been possible to identify Investment opportunities that satisfy the portfolio’s objective in the secondary market for hedge fund units, where imbalances between the number of buyers and sellers of these units have allowed Ferd to purchase units below their estimated value.

Ferd Special Investments reported a return of NOK 225 million in 2014, approximately equivalent to a 10% return.

The portfolio produced a good return in 2014, principally as a result of distributions made by funds in the portfolio. The portfolio was valued at year-end at NOK 2.3 billion.

Ferd Real Estate

2014 was a good year for Ferd Real Estate. Ferd Real Estate reported operating profit of NOK 254 million as compared to NOK 80 million in 2013. Market conditions for real estate as an asset class were good in 2014, due in part to further reductions in interest rates and an improvement in the banks' appetite for real estate lending. The main contributors to the profit reported for 2014 were the good return on a development project at Lysaker on the outskirts of Oslo and the performance of Ferd Real Estate's investments in two European real estate funds.

Ferd Real Estate's value-adjusted equity was NOK 1.9 billion at the end of 2014, with a return on the portfolio of 15% for 2014.

The Tiedemannsbyen project as a whole is for around 1,200 residential units, and will be carried out over a period of between 10 and 15 years. Tiedemannsbyen DA will develop approximately 600 units in the first stage, while in the second stage Tiedemannsfabrikken AS will develop 320 units. Tiedemannsfabrikken AS is owned 50/50 by Ferd Real Estate and Selvaag Bolig, and this collaboration with Selvaag Bolig commenced in 2014.

In 2014, Ferd Real Estate had one office building under construction for Aibel in Bergen. The development is due for completion in the first half of 2015, and Ferd Real Estate decided in February 2015 to sell this building as an investment property.

We anticipate that the commercial rental market will face more challenging conditions in 2015, particularly in areas with clusters of businesses exposed to oil-related activities. We anticipate that rental levels will remain flat in central locations, but expect a slight decrease in rental levels in non-central areas.

2014 was a very good year for the residential real estate market, with high price growth, particularly in major towns and cities. Although increasing numbers of new residential units are being constructed and the unemployment rate is expected to rise slightly, we think the residential real estate market will be shaped by the stable outlook for the Norwegian economy and low interest rates.

Ferd Social Entrepreneurs

Ferd Social Entrepreneurs (FSE) invests in social entrepreneurs who reflect Ferd’s vision of creating enduring value and leaving a clear footprint.

FSE has chosen to apply a focused strategy for its interpretation of what is included in the definition of social entrepreneurship. Social entrepreneurs must play a part in solving social problems while at the same time demonstrating a good likelihood that their activities will be financially self-sufficient over a time horizon of 3 to 6 years. FSE principally supports social entrepreneurs who work with children and young people.

The Board of Ferd Holding AS has allocated up to NOK 25 million annually for work with social entrepreneurship. In addition, Ferd's other business areas and subsidiaries support social entrepreneurs with time and commitment as board members and through other assistance.

Social entrepreneurship is a strongly growing area internationally that is also attracting increasing interest in Norway. FSE is being approached by a large number of parties interested in the area who want to learn from FSE's experience and to collaborate on potential projects. FSE has chosen to prioritise the use of its resources on teams and individuals where we think there is good potential for practical action and benefits that will further the cause of social entrepreneurship.

Health, safety, environmental matters and employment equality

Recent years have seen increasing emphasis on environmental issues in the industrialised countries of the world. None of the group’s activities produces discharges that require licensing and environmental monitoring. Ferd is committed to ensuring that companies it owns operate in a sustainable manner and demonstrate environmental awareness.

Elopak's focus on environmental measures continued in 2014. As part of its target to replace all non-renewable raw materials with renewable alternatives, Elopak launched a new packaging in 2014 based on renewal polyethylene in the coating material and using a screw closure. This represents a milestone in work on reducing the environmental footprint, and is a major step towards making all such packaging 100% renewable. In addition, Elopak has implemented a number of measures to improve the energy efficiency of its production, and has started to phase in a strategy to purchase 'green' energy. Other companies in the group strive to limit their impact on the external environment to the greatest extent commercially possible, this includes waste sorting and proper disposal of specialist waste created by production processes.

The Ferd group had 4,578 employees at the end of 2014, and after including employees of Aibel the total number for 2014 was 9,746. The proportion of female employees in the Ferd group is 27%. Sick leave amounted to 3.5% for the Ferd group in 2014. The working environment at Ferd AS is considered to be good. Ferd AS had 38 employees at the close of 2014, of which 23 are male and 15 are female. The Board of Directors of Ferd AS comprises one female director and four male directors. No serious accidents or injuries were reported at Ferd AS in 2014. For the group as a whole, there were no accidents that led to loss of life, but there were isolated cases of injuries at work that resulted in short periods of sick leave.

It is the company’s policy to treat female and male employees equally. This is reflected in a policy of equal salaries for equal responsibilities, and a recruitment policy that emphasises the selection of candidates with the right expertise, experience and qualifications to meet the requirements of the position in question. The company strives to be an attractive employer for all employees, regardless of gender, disability, religion, lifestyle, ethnicity or national origin.

Allocation of profit for the year

It is proposed that NOK 20 million of the profit for the year of NOK 534 million is paid as a group contribution, and that the remaining NOK 514 million is transferred to other equity.

Bærum, 24 April 2015

The Board of Directors of Ferd AS